Retirement Plan 401k

401k is a type of qualified retirement plan as defined under 26 U.S. Code § 401. It’s an employer-sponsored retirement plan that offers tax deferral benefits for its members. This plan ensures a company maintains top talent who are usually keen on retirement goals.

401k is a defined contribution plan and can be either;

401k vs 401k Roth

Traditional Plan

Employee inputs are not factored in when deciding taxable income hence an upfront tax break.

For example, if your salary is $100,000, and you contribute $10,000, your salary will be deemed to be $90,000 for tax purposes.

However, when making an exit, the savings of $10,000 is deemed income, and will not be tax-free.

This plan is highly favored if you are in the middle of your career as your current income is much higher than what you will draw monthly at retirement.

Roth Plan

Employee inputs do not affect taxable income as they will be withdrawn tax-free.

For instance, if your salary is $100,000, and you contribute $10,000, your salary will be deemed to be $100,000 for tax purposes. On the upside, when making a qualified exit, you won’t pay any taxes.

This plan is highly advised if you are at the start of your career because your current income is taxed at a lower bracket than what you will draw monthly at retirement.

Safe Harbor 401K Plans

A Safe Harbor is a specific 401(k) plan that is not discriminatory. (does not favor highly Compensated Employees (HCEs and Executives). In short, all employees must participate in a meaningful manner to maintain their tax status.

How do 401k works

The employee, the employer, or both make monthly contributions at a set percentage to the employee’s individual account in a trust designed to be accessed strictly at retirement. Contributions are usually calculated using a set formula that may be based on average salary and service in years.

The employees make decisions on what to contribute, investment choices, and plan exits.

Operationally, funds are managed by the sponsor(employer) through a professional investment firm. He decides on the type of 401k plan, and investment plans within the scheme.

These are invested and managed in line with federal insurance limitations set through Pension Benefit Guaranty Corporation (PBGC).

Taxes for 401k

401k match contribution is tax-deductible to the employer (26 U.S. Code § 404) and hence deemed a legitimate expense for tax purposes subject to certain limits.

Employees gain as the contribution is deemed deferred wages and not subject to current tax. Also, any gains on Investments made by the 401k are not subject to tax until when it’s distributed out.

Employers use different methods to match employees’ contributions up to a certain percentage.

Is 401K a Defined Benefit Plan or a Defined Contribution Plan

The Defined benefit plan promises a fixed (specified) amount on retirement in dollars.

401k does not guarantee a fixed amount at retirement, rather the employee, employer, or both contribute a specific amount to an employee’s account.

The sponsor(Employer) appoints a Professional Investment Manager to run the investment side of the 401k plan. And this makes the 401k a Defined contribution plan.

Rules for 401k

These are the rules and regulations controlling your contributions, withdrawals, and taxes on savings in 401k. Basically, they cover;

-

Eligibility

A 401k plan cannot discriminate on participation e.g. require eligibility based on the date of joining.

-

Qualified Retirement Plan

Contributions by the employee are tax-exempt in that year of income (except for 401k Roth plans). Employee effectively defers this income until retirement.

-

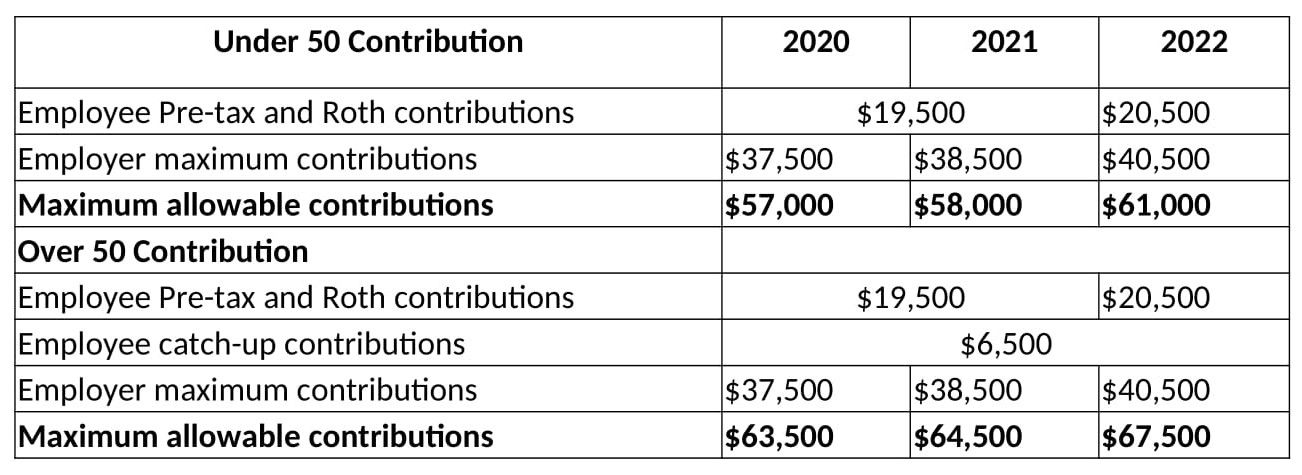

Maximum contributions

In 2022, most employees can contribute up to $20,500($19,500 in 2021). Again, Highly compensated employees (HCEs) who earn more than $135,000($130,000 in 2021) may only access the maximum contribution of $20,500 if lower-paid employees participate in the retirement plan.

HCEs cannot contribute any more than 2% of their salary in comparison to Non-HCE e.g. if Non-HCE contributes 2% of their salary, then HCEs can only max 6%.

Employees over 50 years can contribute an extra $6,500. HCEs over 50 years can participate if the plan allows it.

-

Employer 401K matching contributions

The employer enjoys full discretion. At the moment, he can only contribute to a maximum of $40,500($38,500 in 2021)

-

401K Vesting

Vesting means ownership. Vesting occurs immediately for the employees’ portion, while the employer’s portion may vest immediately or over time.

Varies from plan to plan. It is advisable to refund all loans in full. The taxman treats defaults the same as exits and will penalize them.

-

401k withdraw rules

Taxman considers this as ordinary income and hence taxable. Exits could be for a variety of reasons including retirement, loss of job, or incapacitation.

Early exits (before age of 59½ years) may trigger penalties and taxes.

-

Penalty-free Withdrawals

It’s not easy to withdraw money from your traditional 401k without incurring penalties on top of taxes if under 59½ years. Exceptions only exist for hardship exits.

However you can access your Roth plan tax-free, but the 10% penalty still applies if accessed before the age of 59½ years, or not had the account for at least 5 years.

If you happen to withdraw before age of 59½ years, the taxman considers this early exit and you may be subject to a 10% penalty.

-

401 K withdrawal without Penalty

-

Substantially equal periodic payments (SEPPs)

When required to access a certain amount annually from your 401k for at least five years from or until you reach the age of 59½ years, whichever is earlier -

401k rules at 55

Police and Firemen can access penalty-free withdrawals at the age of 50. Other retirees can access this at age 55 or older. -

Qualifying medical expenses

The taxman can grant you access to your 401k if your medical expenses exceed 10% of your adjusted gross income (AGI). This will not trigger any penalties. -

Permanent disability

You can access your 401k without penalty if you develop any disability that prevents you from seeking employment indefinitely. -

Qualified domestic relations order

You can withdraw penalty-free Under a Court order to pay off your divorced partner. -

401K loan

You can access your savings through a loan. A 10% penalty is charged in case of default as the taxman considers this an exit.

Mandatory exits from a 401k are required by the IRS once a member attains the age of 72, failure to which the member faces stiff penalties. (watch out for a potential 50% penalty on Required Minimum Distributions (RMDs)).

-

Cashing out

This differs by plan, administrator, and employer. Not every employer allows access before retirement. Ideally, the longer you wait to exit the better off you are.

The taxman considers any exit before 59½ as early access.

-

401k rollovers rules

Your savings can be rolled to an IRA on request to the 401K administrator. This does not attract the 10% penalty, however, a one-time transfer fee is applicable.

-

Elective salary deferrals

Taxman excludes this portion from taxable income (the exception being savings to designated Roth deferrals).

-

401k distributions rules

The taxman considers any outflows from the scheme as taxable income (except for some qualified access to designated Roth accounts).

401k Maximum Contribution

The taxman caps maximum inputs periodically. This caters to inflation and other factors. The maximum rate for 2022 was $ 67,500($64,500 in 2021).

401k Maximum Contribution for Highly Compensated Employees

Highly Compensated Employees (HCEs) face a limit on their inputs to most 401(k) plans unless the plan is a Safe Harbor 401k.

Secondly, HCEs cannot save more than 2% more of their salary on the plan as compared to the average non-HCE contribution. (if the average non-HCE employee saves 5%, the HCE cannot go beyond 7% of their salary).

IRS deems you an HCE if you score any of the three;

- If you own more than 5% of the company

- Or took home more than $135,000 in the previous year

- Or among the top 20 most paid in the company

Contributions above set limits by HCEs may lead to the plan losing its tax status. Although, this can be resolved by joining a second plan not related to the current employer e.g. traditional IRA.

Bottom line

Cashing out is not the best option as it triggers penalties and taxes. It also increases the risk of heading into retirement without finances.

Cashing out also takes time, some small firms only do quarterly or early allocations. Read and understand the rules of the plan.

Leave a Reply

You must be logged in to post a comment.