What is a credit card interest rate

What does credit card APR mean

APR for credit cards is the interest rate you pay for balances after the due date as per your billing cycle- simply put, it’s interest paid for borrowing money on some credit account (cost of borrowing).

APR indicates how expensive a transaction will be compared to each one and It’s typically stated as a yearly rate (Annualized) hence the Annual Percentage Rate (APR).

While interest rate and APR might not have the same meaning when borrowing other types of loans, for credit cards, they typically have the same meaning.

Why is credit card APR important

It often comes into focus if you carry over your credit card balances. APR rate gives you a clear picture of how much you will pay when you borrow through your credit card hence an important tool when making comparisons and other financial decisions.

It’s also worth noting that other transactions like Credit card cash advances, and credit card late payments might be subject to steep APR than the rate charged on normal credit card balances.

Credit card APR includes all fees included in accessing the credit giving you an idea of how costly the borrowing will be.

Types of Credit Card APR

Fixed APR

This is a type of APR that is not pegged on any index (U.S. Prime Rate-Published in the Wall Street Journal), hence it doesn’t automatically rise or fall depending on the index. However, the rate can be adjusted by the issuer subject to notice (60 days) and as per other Federal restrictions (CARD Act). Terms and conditions are usually changed after 45 days’ notice.

- The major pro is that it’s fairly straightforward as the rate is fixed.

- The major con is that these cards are a little hard to find

Variable APR

This type of APR is tied to the prime rate. When the U.S. Prime Rate changes, the APR rate steadily fluctuates along with the Prime Rate.

- A major pro is if balances are paid on time and in full, it won’t affect you

- The major con is its increase along with other indexes and could potentially increase your costs in the long run

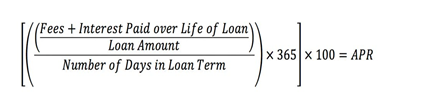

How is Credit Card APR Calculated

This is a simplified method of APR calculation.

Let’s assume you borrow $1,000 that is charged $25 on origination and for 180 days. The interest charged is $75 for the entire period. What is the APR?

- Start by determining the total cost of the borrowing ( Interest plus Origination Fee)

| $75+$25=$100 |

- Then, Divide the total cost of the loan by the amount borrowed

| $100/$1,000=0.1 |

- Then, dived results from 2 above by the term of the borrowing

| 0.1/180= 0.00055556 |

- Multiply the result in 3 above by 365

| 0.00055556×365= 0.2027778 |

- Lastly, convert results in 4 above to percentage format

| 0.20277778×100=20.28% |

All this is summarized in the formula below;

Types of credit card APR

Introductory/Promotion APR

It’s a special interest rate offered on a promotional basis, sometimes as low as 0% APR. It’s used to attract new customers to a new card. After the expiry of the introductory offer, it reverts back to variable APR, which will be determined by your credit score.

Purchase APR

It’s the interest rate you will be charged on your credit balances after the grace period. This interest will be charged every time you use your card and don’t clear the balance at the end of the billing cycle. It’s best avoided by paying off balances in full after the billing cycle.

Cash Advance APR

This applies when you borrow from your credit card in cash. This rate is typically higher than your normal purchases and doesn’t have a grace period.

Penalty APR

This is usually triggered by missed or returned payments. It can go as high as the maximum rate on the agreement (average 29.9%) This may last as long as six months after catching up with payments.

Balance Transfer APR

This is the rate applicable when a credit account is transferred from one credit card to another.

It’s a good strategy for managing cyclical consumer debt since it swaps from high APR to lower APR cards

How to lower Credit Card APR

The lender decides on the rate, technically you can’t do much. However, several other factors might also influence the appraisal when determining the rate. This includes;

Credit Card Credit Scores

People with good credit scores tend to get lower interest rates as compared with people with poor scores. For the same credit score, the Key is to shop around and compare different rates offered by different issuers. Please remember payment history makes up around 35% of credit scores, always pay your bill on time.

Type of credit card

Understand the terms and conditions of your card, especially the pricing section. You should also target cards with lower introductory APR offers. Cards with a 0% APR introductory offer are a good way of financing larger purchases that may take longer to repay. Be mindful when doing this purchase as the 0% APR will expire after the introductory period and you will be back to variable APR.

Credit Utilization

This will have a direct effect on your credit card APR. Credit raters consider a card Holder to be risky if they tend to utilize more than 30% of their credit

Payment History

You can lower your APR by directly negotiating with the Issuer. This may need showing proof of timely payments and evidence of having low APR on other cards in your name. Payment history is a good indicator of abiding by future payments.

What is a good APR rate for Credit Cards

Financial situations vary from one person to the next and most credit cards have variable APR. This means that there is no specific answer to what constitutes a good APR.

Factors that affect the APR include credit scores, type of loan, or type of card. Consider anything between 14%-16%(federal Reserve-2021) as a ‘good’ APR.

Always look for anything below the lower national average. Remember, Lower is always better, any card with 0% APR is always the best.

Bad credit scores can generate as high an APR as 25%.

People with subpar credit scores are usually the targets of cards with high APR. This is so because they are looking to shore up their credit scores. Enrolling in cards with such high APRs is usually a recipe for consumer debt cycles as the rate is unsustainable. The trick would be to spend and pay off any balances in full at end of the billing cycle.

Bottom line

It’s important to understand how APR affects your costs, especially when financing a purchase that its payment will go beyond the grace period or when acquiring a new credit card.

As much as low-interest rates may be the deciding factor, the APR points out the exact damage to your wallet.

Leave a Reply

You must be logged in to post a comment.