What is Medigap

Medicare Supplement Insurance, also known as Medigap, is a private health insurance plan that helps fill the coverage ‘gaps’ (standardized benefits- costs for Original Medicare or outside the scope) in the Original Medicare (Part A and B).

Original Medicare will pay first for a big part (around 80%) of the medical costs, but not all. Medigap (which by the way doesn’t work with Medicare Advantage) may cover the outstanding costs (about 20% of Medicare). This includes;

- Copayments

- Coinsurance

- Deductibles

- Hospital costs incurred after running out of Medicare-covered days

- Skilled nursing facility costs incurred after running out of Medicare-covered days

You must have enrolled in Original Medicare to qualify for a Medigap Plan (most cover 20% of what’s not covered by Parts A and B).

Medigap may also cover health care costs that original Medicare does not cover at all like care received when traveling outside of the U.S.

Medicare Supplement also works with a standalone Part D Prescription Drug plan.

Types of insurance that are not Medigap plans:

- Medicare Advantage Plans e.g. HMO, PPO Plans, or Private Fee-for-Service Policies.

- Medicare Prescription Drug Plans

- Medicaid

- Employer or union plans e.g. Federal Employees Health Benefits Program (FEHBP)

- Tricare

- Veterans’ benefits

- Long-term care insurance policies

- Indian Health Service, Tribal, and Urban Indian Health plans

Here’s how Medigap works

- Member pays a monthly premium for their Medigap.

- In return, Medigap pays most of the out-of-pocket expenses (roughly 20 percent is coinsurance/Copay required by Medicare. With some Medigap plans).

Medicare Advantage plans can also supplement Medicare as well. They are in a good position to offer additional health coverage that Medigap doesn’t.

What’s covered by Medigap

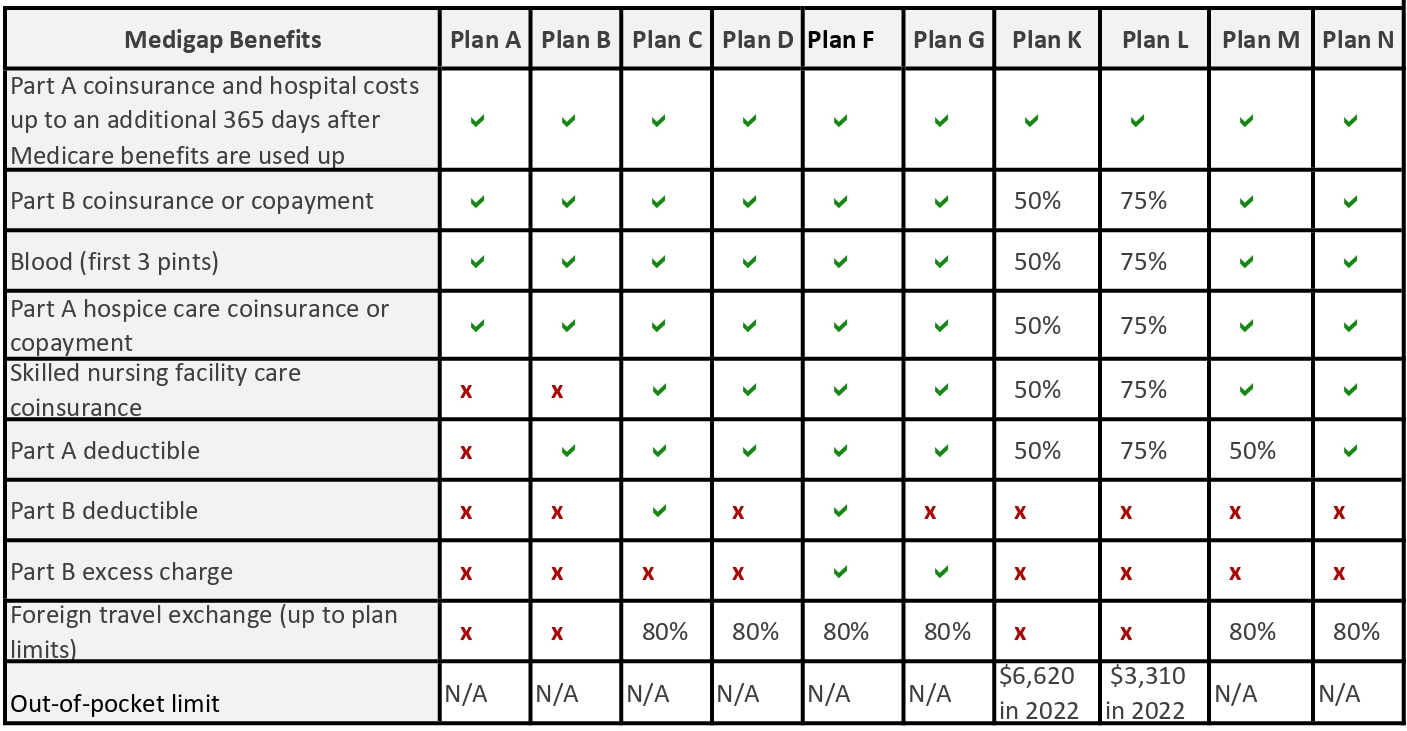

Medigap plans may cover all medical and hospital care. This cost includes (with a few exceptions):

- Coinsurance and hospital care(Part A will cover up to additional 365 days after the exhaustion of Medicare benefits)

- Copayment or coinsurance(Part B)

- Blood (for the first three pints)

- Coinsurance/copayment paid for hospice care (Part A)

- Coinsurance costs for skilled nursing care (Plans A and B do not cover)

- Deductibles for both Plan A and Plan B

- Part B excess charge (Only covered by Plans F and G)

- Foreign travel exchange (Only covered by Plans A, B, K, and L)

- Plans K and L will provide 100% coverage for the rest of the calendar year after the out-of-pocket limit and Part B deductibles are met.

Medicare will cover its rightful share of Medicare-approved healthcare costs. Then, the Medigap plan will then cater to its share of the coverage (Standardized benefits).

Medigap plan chart

What’s not covered by Medigap

Medicare Supplement plans generally do not cover the following services:

- Vision or Dental coverage (may be offered separately with low-cost monthly premiums.)

- Eyeglasses

- Hearing aids

- Long-term care or Private-duty nursing (this is non-skilled care in nursing homes).

- Prescription drug coverage(may be offered separately with low-cost monthly premiums.)

- For preexisting conditions, sometimes, Individuals may be required to cover their own costs. Medigap will provide coverage thereafter.

Medigap Eligibility

You are eligible for Medicare Supplement Insurance if:

- Aged 65 or older and

- Enrolled in Original Medicare Part B

Medigap Plan 2020

Currently, Private insurance companies offer up to 10 standardized Medigap plans.

They have letter names A through to N (A, B, C, D, F, G, K, L, M, and N- policies in Wisconsin, Massachusetts, and Minnesota have the same albeit different naming).

Each insurance company has the liberty to decide which Medigap plan to offer, although state laws affect which ones they have to offer.

Companies that sell Medigap plans:

- Don’t have to sell every Medigap plan

- However, they Must offer Plan A, if they are offering any Medigap policy

- Also, they Must also offer Plan C or Plan F if they offer any plan

Please Note: individuals eligible for Medicare on or after January 1, 2020, will not be able to buy coverage that pays for the Part B deductible. This is inclusive of Plan C and Plan F.

Individuals who qualified before this date will still be able to purchase Plan C or Plan F.

Medigap Plan 2022

- Medigap high deductible plan F: In some states, Plans F and G do offer a high-deductible plan. With this option, an individual will foot the bill for coinsurance, copayments, and deductibles up to $2,490 (in 2022) before plan coverage kick in.

- Plans K and L: will provide 100% coverage for the rest of the calendar year after meeting your out-of-pocket yearly limit and the yearly Part B deductible.

- Plan N covers 100% of the Part B coinsurance, except for a copayment of up to $20 for some office visits and up to a $50 copayment for any emergency room visits that do not lead to inpatient admission.

Medigap Enrollment Periods

You can enroll in Medicare Supplement plan at any time throughout the calendar year.

Individuals also have a 6-month one-time open enrollment period (best enrollment period), to get coverage from any policy offered in their state with guaranteed coverage for pre-existing conditions.

After this one-time open enrollment, you may be ineligible to purchase a Medigap plan or if eligible will have to pay a lot more.

This one-time open enrollment is applicable as follows;

- For individuals who have retired at 65 and have or are applying for Medicare Part B, the open enrollment period will be 6 months from the first day Part B coverage begins.

- For individuals who are 65 but not yet on retirement and have work-based coverage, open enrollment will be when they retire and sign up for Part B coverage.

- If your spouse is already in another group of health care coverage and you are not ready to enroll in Part B, you can apply later and without penalties during a Special Enrollment Period after the Initial Enrollment Period has expired.

This plan is also available to individuals younger than 65 and eligible for Medicare due to disability.

Plan C Medigap

What Is Medicare Advantage (Part C)

Medicare Advantage also called “Part C” or “MA plans.” is a type of Medicare-approved plan provided by private insurance companies. It’s a Private alternative to Medicare Original Parts A (hospital insurance) and Medicare Parts B (medical insurance).

It provides all benefits of Medicare Part A and Part B (Original Medicare), plus some additional coverage( Part D prescription drug coverage, dental, vision, and hearing care), under one policy. After enrollment medical bills are covered by the insurance company rather than by Original Medicare.

What is covered under Medicare Advantage Plan

Medicare Advantage offers the exact same, if not better, coverage as Parts A and B.

It’s required to provide coverage offered by Original Medicare (Part A and Part B), this will include:

- In-patient care

- Skilled nursing facility care

- Nursing home care

- Hospice care

- Home health care

- Clinical research

- ER services

- Durable medical equipment (DME)

- Mental health services (Inpatient and outpatient)

- Limited outpatient prescription drugs

Medigap Plan Comparison

Medicare Supplemental Insurance options

Medicare Supplement Insurance is different from Medicare Advantage. You can only have one of the plans not both..

What is the difference between Medigap and Medicare’s advantage

| Medicare supplement | Medicare Advantage (Plan C Medigap) |

| Has One open period per lifetime unless under special circumstances | Ha two open enrollment periods in a year |

| Charges monthly premiums | Monthly premiums can be as low as $0 |

| Members may be provided with up to three different insurance cards. | Only one insurance card is issued. |

| Pays only for Original Medical and Does not cover Part D prescription drug coverage. Members will need to coordinate between Medicare, Medigap plan, and their separate Part D prescription drug plan. | It’s possible to have one cover that coordinates all care. It’s possible to have one cover that coordinates all care. Most policies include Part D prescription drug coverage, and some include vision, hearing, and dental coverage |

| Coverage meant for one individual—spouses have to buy separate coverage | May cover spouses |

| Covers in and out of in-network providers. You can see any MD or Physician that accepts Medicare. | Some plans do not provide coverage for out-of-network care. |

To access Medicare supplements or Medicare Advantage plans, you must also be enrolled in Medicare Part A and Part B

Also, the Medicare Supplement plan is not the same as a Medicare Advantage plan.

Medicare Advantage plans offer Medicare benefits and follow Medicare rules (coverage may include drug coverage).

Medicare Supplemental plans are designed to fill gaps in what your Medicare plan does not cover.

Medigap costs

The average premium for Medigap in 2022 is approximately $150 per month or $1,800 per year.

Costs will vary across states and by insurance company (some plans have a high-deductible option) with the main determinant being your location and age.

Always remember, the same plan that might look less expensive at age 65 might be very costly at age 85. It’s in your best interest so ask the insurance provider how they determine their premium pricing.

Pricing is determined in three ways:

- Community-rated(Not age-related): same monthly premium is levied across all members that have access to the Medigap plan, regardless of age.

- Issue age-rated/Entry age-related: monthly premium is based on how old you are at the time of purchase. Younger members tend to pay lower premiums. The premium costs based on this type of rating will not go up due to age, but rather due to inflation or other factors.

- Attained age-rated: The monthly premiums are tied to your current age and increase as you get older. Premiums will always start at the lowest since you are young, but have the potential to hit the roof when impacted by inflation and other factors.

Bottom line

- There is no limit to what is paid as copayments coinsurance or deductibles in a coverage year. It’s worth having access to secondary coverage such as a Medigap or Medicare Advantage plan to help with gap coverage.

- Members can renew any standardized Medigap policy despite having underlying health conditions (guaranteed to be renewed). No insurance company can cancel this policy as long as the premium is paid (Federal protections for people over 65). However, in rare cases, Medigap may exclude coverage for prior medical conditions for a limited amount of time.

- If you are dropping your Medigap policy, be mindful of the timing of joining a new Medicare drug plan as you may be liable to pay a late enrollment penalty. This is applicable if one of these conditions applies to you:

- You have dropped the entire Medigap policy and the drug coverage was not creditable prescription drug coverage

- You go for 63 days consecutively or more before your new Medicare drug coverage begins

Leave a Reply

You must be logged in to post a comment.